Q2 Data Show CUs In U.S. Rapidly Approaching $1.5 Trillion In Assets

ALEXANDRIA, Va.–Data for federally insured credit unions as of mid-year 2018 show total assets rapidly approaching $1.5 trillion even as the smallest credit unions continue to decline.

NCUA’s Quarterly Credit Union Data Summary show that as of June 30, 2018, there were 5,480 federally insured credit unions with 114.1 million members.

Here’s a look at how FICUs performed overall:

- Total assets in federally insured credit unions rose by $79 billion, or 5.8%, over the year ending in the second quarter of 2018, to $1.43 trillion.

- Total loans outstanding increased $89 billion, or 9.8%, over the year to $1.0 trillion. The average outstanding loan balance in the second quarter of 2018 was $15,226, up $611, or 4.2%, from one year earlier.

- The delinquency rate at federally insured credit unions was 67 basis points in the second quarter of 2018, down from 75 basis points one year earlier. The net charge-off ratio was 60 basis points, up from 57 basis points in the second quarter of 2017.

- Insured shares and deposits rose $56 billion, or 5.2%, over the four quarters ending in the second quarter of 2018, to $1.13 trillion.

- The loan-to-share ratio stood at 83.0% in the second quarter of 2018, up from 79.7% in the second quarter of 2017.

- The credit union system’s net worth ratio was 11.01% in the second quarter of 2018, compared with 10.80% one year earlier.

- Net income totaled $12.7 billion at an annual rate in the second quarter of 2018, up $2.5 billion, or 24.8%, from the same period a year ago.

- The net interest margin for federally insured credit unions was $43.2 billion in the second quarter of 2018, or 3.1% of average assets. That compares with $38.7 billion, or 2.9% of average assets, in the second quarter of 2017, NCUA said.

- The return on average assets for federally insured credit unions was 90 basis points over the year ending in the second quarter of 2018, up from 77 basis points in the second quarter of 2017. The median return on average assets across all federally insured credit unions was 52 basis points, up 15 basis points from the second quarter of 2017.

- The number of federally insured credit unions declined to 5,480 in the second quarter of 2018, from 5,696 in the second quarter of 2017. In the second quarter of 2018, there were 3,444 federal credit unions and 2,036 federally insured, state-chartered credit unions. “The year-over-year decline is consistent with long-running industry consolidation trends,” the agency said.

- The number of credit unions with a low-income designation rose to 2,544 in the second quarter of 2018 from 2,524 one year earlier.

- Federally insured credit unions added 4.8 million members over the year, and credit union membership in these institutions reached 114.1 million in the second quarter of 2018.

Individual Asset Categories

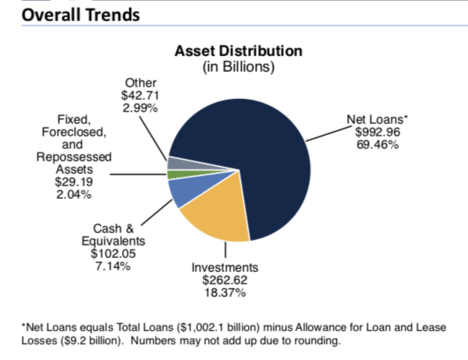

- Cash and equivalents (assets with maturity of three months or less) declined $2.4 billion, or 2.3%, to $102.1 billion.

- Total investments (instruments with maturities in excess of three months) fell $12.1 billion, or 4.4%, to $262.6 billion.

- Investments with maturities of less than one year declined $5.4 billion, or 6.9%, to $72.2 billion.

- Investments with maturities of one to three years declined $3.2 billion, or 3.6%, to $87.0 billion.

- Investments with maturities of three to five years declined $5.1 billion, or 7.2%, to $65.5 billion.

- Investments with maturities of five to 10 years rose $2.1 billion, or 6.7%, to $34.0 billion.

- Investments with maturities greater than 10 years fell $0.5 billion, or 11.8%, to $4.0 billion.

- Total loans outstanding increased $89.1 billion, or 9.8%, over the year to $1.0 trillion. Credit union loan balances rose over the year in every major category, compared with the second quarter of 2017.

- Loans secured by 1- to 4-family residential properties totaled $430.7 billion in the second quarter of 2018; data are unavailable prior to 2017Q3.

- Auto loans increased $33.7 billion, or 10.6%, to $352.0 billion. Used auto loans rose $19.2 billion, or 9.9%, to $212.7 billion. New auto loans rose $14.6 billion, or 11.7%, to $139.4 billion.

- Credit card balances rose $4.9 billion, or 9.1%, to $57.9 billion, NCUA said.

- Non-federally guaranteed student loans rose $0.6 billion, or 14.2%, to $4.6 billion.

- Commercial loans, excluding unfunded commitments, totaled $67.7 billion in the second quarter of 2018; data are unavailable prior to 2017Q3. Commercial loans are not directly comparable to member business loans, the agency noted.

Delinquencies & Charge-Offs

The delinquency rate at federally insured credit unions was 67 basis points in the second quarter of 2018, down from 75 basis points one year earlier.

Loan performance improved in most categories, NCUA said.

- The delinquency rate on fixed real estate loans was 40 basis points in the second quarter, down from 47 basis points one year earlier.

- The credit card delinquency rate was 115 basis points, up from 108 basis points in the second quarter of 2017.

- For auto loans, the delinquency rate was 55 basis points in the second quarter of 2018 compared with 59 basis points one year earlier.

- The delinquency rate for commercial loans, excluding unfunded commitments, was 132 basis points in the second quarter of 2018; data for quarters prior to 2017 Q3 are not available.

- The net charge-off ratio for all federally insured credit unions was 60 basis points in the second quarter of 2018, up from 57 basis points in the second quarter of 2017.

Liabilities and Net Worth

- Credit union shares and deposits rose by $62.1 billion, or 5.4%, over the year to $1.21 trillion in the second quarter of 2018. Regular shares rose $27.3 billion, or 6.5%, to $446.6 billion. Other deposits increased $21.0 billion, or 3.7%, to $581.6 billion, led by share certificate accounts, which were up $14.9 billion, or 7.2%, and money market accounts, which rose $4.8 billion, or 1.9%.

- The credit union system’s net worth increased by $11.5 billion, or 7.9%, over the year to $157.4 billion. The aggregate net worth ratio — net worth as a percentage of assets — stood at 11.01% in the second quarter of 2018, up from 10.80% one year earlier, according to NCUA.

Income Statement Details

- Net income for federally insured credit unions in the second quarter of 2018 totaled $12.7 billion at

an annual rate, up $2.5 billion, or 24.8%, from the second quarter of 2017. Interest income rose $6.1 billion, or 13.3%, over the year to $51.8 billion, and non-interest income increased $2.2 billion, or 12.6%, to $19.8 billion. - Interest expense totaled $8.7 billion annualized in the second quarter of 2018, up $1.7 billion, or

23.5%, from one year earlier. Non-interest expenses grew $3.1 billion, or 7.8%, over the year to $43.5 billion in the second quarter. Rising labor expenses, which were up $1.5 billion, or 7.4%, accounted for half of the increase in non-interest expenses. - The aggregate net interest margin widened by $4.4 billion over the year, or 11.5%, to $43.2 billion at an annual rate in the second quarter of 2018.

- The credit union system’s provision for loan and lease losses rose $1.0 billion over the year, or 17.5%, to $6.7 billion at an annual rate in the second quarter of 2018.

Long Running Trends in Assets

“Consistent with long-running trends, credit unions with assets of at least $1 billion reported the strongest growth in loans, membership, and net worth over the year ending in the second quarter of 2018,” NCUA noted in its analysis. “Credit unions with less than $100 million in assets reported declines in loans, membership, and net worth over the year.”

Other Data Points:

- The number of federally insured credit unions with assets of at least $1 billion increased to 302 in the second quarter of 2018 from 282 in the second quarter of 2017. These 302 credit unions held $926.2 billion in assets, or 65% of total system assets. Credit unions in this category reported loan growth of 13.7%. Membership rose 9.6%. Net worth increased 11.9%.

- The number of federally insured credit unions with assets of at least $500 million but less than

$1 billion increased to 240 in the second quarter of 2018 from 238 in the second quarter of 2017. These 240 credit unions held $169.7 billion in total assets, or 12% of total system assets. Credit unions in this category reported loan growth of 2.5%. Membership edged up 0.4%. Net worth increased 3.1%. - The number of federally insured credit unions with at least $100 million but less than $500 million in assets declined to 1,034 in the second quarter of 2018 from 1,046 in the second quarter of 2017. These 1,034 credit unions held $233.1 billion in total assets, or 16% of total system assets. Credit unions in this category reported loan growth of 3.5%. Membership declined 1.8%. Net worth increased 1.6%.

- The number of federally insured credit unions with at least $50 million but less than $100 million in assets fell to 709 in the second quarter of 2018 from 732 in the second quarter of 2017. These 709 credit unions held $51.0 billion in total assets, or 4% of total system assets. Credit unions in this category reported a 0.1% decline in total loans. Membership fell 4.7%. Net worth edged up 0.2%.

- The number of federally insured credit unions with assets of at least $10 million but less than $50 million declined to 1,731 in the second quarter of 2018 from 1,813 in the second quarter of 2017. These credit unions held $43.4 billion in assets, or 3% of total system assets. Credit unions in this category reported a 0.7% decline in loans. Membership declined 6.3%. Net worth declined 1.4%.

- The number of federally insured credit unions with less than $10 million in assets declined to 1,464 in the second quarter of 2018 from 1,585 in the second quarter of 2017. These credit unions held $6.1 billion in assets, or less than 1.0% of total system assets. Credit unions in this category reported a 4.5% decline in loans. Membership fell 9.1%. Net worth declined 4.6%.